Have You Ever Wondered If You Can Retire, Stay Retired, and How Much You Can Safely Spend Without Running Out of Money?

Perhaps I can help. My name is Michael Paulding Thomas. I'm a German-American independent Investment Advisor and Securities Principal. Since 1989 I've helped over 200 clients build a "retirement machine" that gives them a lifetime guaranteed monthly income to ensure they don't outlive their money in retirement.When you think of your retirement, does it seem more probable that you will outlive your money or that your money will outlive you?Here's what I offer: a no-cost, no-obligation second opinion to help you figure that out.If you're open to it, I'd like to have relaxed and easy-going conversation with you about your retirement plan. If I think your investments continue to be well-suited, I'll gladly tell you so, and be on my way.If, on the other hand, I think some of your strategies no longer align with your Golden Years, I'll explain why in plain English and recommend some alternatives.

Photo: AylaBaha.com

For the last two decades I've published my popular monthly client newsletter. It includes Nick Murray's Client's Corner, the financial-tip-of-the-month, financial book-of-the-month, podcast-of the-month, video-of-the-month, and much more.If you subscribe, I will start by sending you a series of approximately 25 emails over the course of twelve weeks introducing you to my financial philosophy and the kind of work that I do. Other than that, you will only receive my monthly client emails ― I will not use your email for any other purpose nor share it with others.

My Articles & Essays

Recommended Books

With over three decades in the Investment Advising business, I can attest that this is the simplest and most effective investment book I’ve ever read.If this book resonates with you, then you’ll enjoy working with me. If it doesn’t, you won’t.

For nearly 30 years, financial economist and investment writer Mark Skousen has been collecting all the old wise adages, proverbs, and legends on Wall Street, based on in-depth interviews with old timers, reading rare financial books, and his own experiences in the financial markets. Maxims of Wall Street is the closest thing to Wall Street scripture ever created.“Love you great little book. I plan to shamelessly steal some the lines.” ―Warren Buffett“Beautifully bound collector’s item. It should be on every investor’s bookshelf and read regularly.” ―Bert Dohmen, The Wellington Letter

This is a collection of quotes and thoughts from some of the world's greatest investors.This is a free PDF - just click the image to open it.

The best book on the history of Capital Group. Find out what makes American Funds so special.“Capital, the parent firm of American Funds, is one of the finest business organizations in American Business. This book was written by an index fund/no-load proponent who was looking to debunk American Funds (which are neither indexed, nor no-load) and instead he discovered their exceptional values, performance and pricing. This story is fast-paced and highly interesting, both to Advisors and clients.” ―from the forward of the book.

The Surprising Secrets of America's Wealthy. One of the best books I've ever read on personal financial success.

How the less affluent have fallen into the elite luxury brand trap that keeps them from acquiring wealth and details how to get out of it by emulating the working rich as opposed to the super elite.

Podcasts

This is my favorite investing podcast from my favorite management company.Want to learn how professional investors do it? The weekly, 30-minute Capital Ideas / American Funds audio podcast brings you the latest investment thinking from Capital Group. Each episode gets inside the minds of portfolio managers, analysts and economists to break down market trends, macroeconomic forces, investing approaches and lessons learned from personal experience.

Capital Conversations is a Capital Ideas video podcast offering an unscripted look into The Capital System.Join Mike Gitlin (CEO of Capital Group) as he hosts in-depth discussions with Capital Group's portfolio managers, analysts and senior leaders from around the globe. Gain unique perspectives on investment strategies and market trends while getting to know the people behind the portfolios.

My Past Client Newsletters & Client Letters

This is an index of my monthly client newsletters. I've been writing these since 1989, but have only archived them starting with issue #140. I hope them bring you some value. Also, since 2017 I've added mid-year and year-end letters to my monthly newsletter where I review the principles of our investment philosophy and a brief commentary on the current market.

2017 - 2022

- Year-End Letter 2017

- Year-End Letter 2018

- Year-End Letter 2019

- Mid-Year Letter 2020

- Year-End Letter 2020

- Mid-Year Letter 2021

- Year-End Letter 2021

- Mid-Year Letter 2022

- Year-End Letter 2022

2023

2024

Financial Calculators & Links

This essay started over 36 years ago when I entered into the investment business and began cataloging my beliefs and insights. Eventually I shared it with a few clients (on physical paper!) when they asked for a brief summary of my financial philosophy, strategies and service model. What you're reading here is the most current edition of my original notes.

My Process

Getting Started: 4-Step Process

Step 1We'll have a candid, relaxed and easy-going conversation about your retirement, and any other investment goals you have. I'll explain my philosophies and strategies.(You can schedule a convenient time here.)After our conversation you're going to come to one of two conclusions:.A) "I could probably do this myself." Or, "I don't really like Michael." Or "His concepts don't make sense to me." That's not my favorite option but it's totally fine!B) "I like what I'm hearing and Michael's ideas resonate with me. I want to see what he can do for me." If this is you, then we'll move to Step 2.

Step 2I will collect the information and documents from you I need to create an easy-to-understand plan that is the most efficient, most effective, least complex, and least expensive way to accomplish what you want.

Step 3After I design the plan I'll explain it to you plain English. I'll walk you through the different retirement accounts and ensure you're contributing the right amounts to the right places so that you don't just retire, but you stay retired with a sustainable monthly income designed to weather market swings and rising costs.

Step 4If my plan resonates with you we will complete the paperwork to get your account(s) set-up. If needed, I will do all of the behind-the-scenes legwork of contacting your old accounts to facilitate the transfers.

I will do my utmost to keep the process quick, simple and as painless as possible for you.

My Follow-Up & Service Model

1. First and most important, please don't hesitate to call, email or schedule a time with me for any reason whatsoever. I commit to returning your emails, calls, and voicemails within 24 hours. Note: all account-specific, product-specific and Advice needs to be communicated via email or phone, not text.

2. Next, I’ll certainly call/email if something is going on that’s important enough to require a decision of some sort. This will rarely happen, as our whole philosophy is based on not reacting to current events in the economy or the markets.

“Nothing that happens in 90 days can have any bearing on a long-term investment plan.” ―Nick Murray

3. Once a month I will email my client newsletter which includes the current month's Nick Murray's Client's Corner (must read!), among other interesting investing content.In the July and January issues I will include my Mid-Year and Year-End Client Letters.

4. Finally, every January I will email a summary of your plan, and most importantly show you the number of shares you own of your mutual fund(s).

Other than that: not much. It’s deliberately relaxed, informal, friendly - but most of all open, in both directions.

My Four Core Principals

1: Counter-Cultural

I have a unique point of view that can be described as going upstream to the traditional financial industry and often times against conventional wisdom. I commit to always tell you the plain, unvarnished truth, especially when you may not want to hear it.Investment Philosophy - I am goal-focused and long-term oriented in an industry that will always be market-focused and short-term performance-driven.Investment Strategy - I believe in historically defensible, broadly diversified equity mutual funds vs the current "hot" du jour investment of the moment. I am data-based and fact-driven.

“Successful investing in counterintuitive.” ―Nick Murray“I’m convinced that everything that’s important in investing is counterintuitive, and everything that’s obvious is wrong.” ―Howard Marks

2: Do What's Right

As the name of this site suggests, putting my clients first has been my guiding philosophy since I started in this industry in 1989.I’m a fiduciary advisor. That means I am legally and ethically obligated to act solely in your best interest. As an independent my loyalty is solely to you, not to any company or product vendor. My goal is to help you build a retirement that truly gives you peace of mind.When I sit with a client I ask myself, "What would I do for myself and my family if I were in this situation?" Then that's what I recommend.Doing what's right includes the way I charge fees. Lower costs for you takes precedence over my income.

“I want to be happy by doing well by doing good.” ―Michael“Don’t sell anything you wouldn’t buy yourself.” ―Charlie Munger“The truth tellers have no competition.” ―Nick Murray

3: Make a Complex Subject Simple

I keep my presentations, explanations, strategies and investments as simple as possible. I don't use fancy jargon nor try to impress you with sophisticated language, charts and graphs. I cut through the industry's noise and complexity and provide a straightforward answer.I can help you make sense of the myriad of retirement accounts and investments.

“You don't pay me for the few minutes it takes me to provide you with my best advice - you pay me for the 36 years it took me to know how.” ―Michael Paulding Thomas“Everything must be made as simple as possible, but no simpler.” ―Albert Einstein

4: Behavioral Coaching

At the end of an investor’s life, 95% of his total lifetime return will come from how the investor behaved. And the primary determinant of that behavior will be the quality of the advice he got, or didn’t get. I believe you will do far better in real life with an empathetic, tough-loving behavioral coach than you will on your own.

“An advisor who can modify your behavior is one of the most important investments you make.” ―Chris Davis, Independent Director at Berkshire Hathaway and Coca-Cola“Without an adequately compensated advisor to help with selection and discipline, the individual investor will simply make all the classic and horrendous mistakes.” ―Nick Murray“People make better decisions with financial advisors.” ―Robert Shiller, Nobel Prize-winning economist“Proper investment strategy is as much of a psychological as an intellectual challenge. It is often best to seek professional help to structure and maintain a well-diversified portfolio.” ―Jeremy Siegel

What I Do & What I Don't Do

| Activity | % |

|---|---|

| Analyzing/interpreting the economy and current events. Timing the market, calling tops and bottoms. Identifying consistently top-performing investments: | 0% |

| Crafting a long-term plan and funding the plan with a long-term equity portfolio: | 20% |

| Coaching clients to continue following the plan through all the cycles of the economy, and all the fads and fears of the market: | 80% |

| 100% |

My Ideal Client

Two Temperaments

1. My expertise is best suited for families who are serious about retiring in complete financial security someday (or those who are already retired and want to ensure they stay that way).2. The clients I most enjoy serving are open to professional relationships and have a genuine desire to be helped, which most reliably manifests as teachability.Because my approach to investing is so very countercultural ― being entirely goal-focused and planning-driven in an environment that is overwhelmingly market-focused and performance-driven ― I am looking for people with the ability and willingness to adopt that approach.If you're interested in delegating retirement planning to an expert so that you can spend time on things that matter most to you then I think we'll work great together.

Investible Assets

Many advisors only work with people who have a substantial amount of wealth. I, however, don't require an asset minimum, so you don't have to be rich to benefit from my advice (I have a quite a number of clients in their teens and 20's).

“Anyone earning more than he is spending is a prospect for managed money.” ―Nick Murray

Geography & Flexibility

Though I reside in Southern California I often work remotely (phone, email, video, etc). In fact, I have more clients outside of California than I do locally. I am licensed in AR, AZ, CA, FL, GE, IN, KA, MI, MN, NC, NV, NY, OK, PA, TN, TX, VA (I can add any state, if needed).

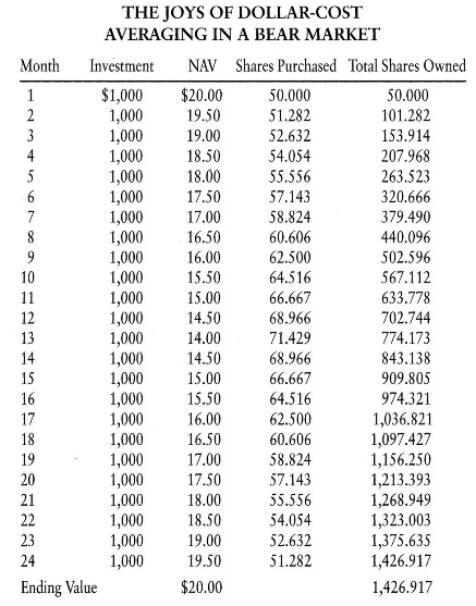

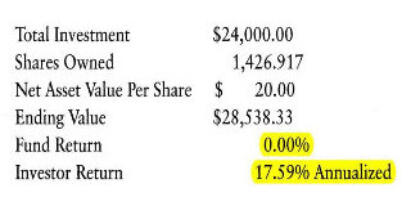

What is Dollar Cost Averaging?

“DCA is stupid-smart.” ―Michael

DCA is an investment strategy designed to reduce volatility in which mutual fund shares are purchased in fixed dollar amounts at regular intervals, regardless of what direction the market is moving. Thus, as prices of securities rise, fewer units are bought, and as prices fall, more units are bought.For example, instead of investing $8,000 into an IRA / mutual fund as a lump sum, the investor buys smaller amounts over a longer period of time ($667 per month). This spreads the cost basis out because you bought mutual funds shares 12-times per year instead of one time.DCA has been called the "dumb man's revenge" because over the long-term it can outperform "clever" market timing strategies and sporadic deposits.

“Dollar-cost averaging is almost real-time re-balancing." ―Nick Murray

“This is a testimony to the genius of dollar-cost averaging, which all long-term accumulators practice because we have no choice: we're investing what we can save from what we earn, and this process is ongoing. Investing over time into a meaningfully diversified equity portfolio, aided by annual re-balancing, inevitably loads up on the laggards and eschews what's hot, thereby insuring that we outperform not just the markets but our own investments." ―Nick Murray

Benefits of DCA

1. It's Smart. Buying more units when prices are low and fewer units when prices are high is a good way to reduce the average cost per unit.2. It's Automatic. With an Electronic Fund Transfer deposits occur systematically from your checking account into your mutual fund. You can do so for as little as $50/month. However, you are always in control - you can increase, decrease, pause, stop and re-start the plan at anytime.3. It's Disciplined. Dollar cost averaging takes the emotion out of investing. You can stop asking yourself, "When's the right time to buy?" It eliminates the issue of market timing. As a result, an investor's returns will be determined more by the overall trend in a given fund as opposed to the investor's specific entry price. In addition, it helps investors reduce their cost basis on securities that decline in value.

“The best time to invest in equities is whenever you have the money. It is the patient, disciplined equity accumulator — looking neither to the left at economic events nor to the right at market gyrations — who achieves his/her lifetime goals. This exquisitely rare accomplishment is never intellectual, but always temperamental.Thus, if I suddenly came into a million after-tax dollars one day, it would all be invested in equities by nightfall. Never having experienced such a day, but instead having spent a career investing my net earnings, I have always been, however haphazardly, dollar cost averaging. That is to say: whenever I had money to invest, and the equity market was terrible, I all unwittingly acquired barrels full of panic-priced shares. And when I had investable sums in soaring markets, I (equally unconsciously) bought thimbleful of relatively overpriced shares.." ―Nick Murray

Nick Murray's 20 Investment Epiphanies

My investment philosophy is based upon the teachings of Nick Murray and Warren Buffet.

Nick Murray is the Advisor to Advisors and prolific author. With 50+ years of experience in the investment markets he is an expert in the art and science of helping individual investors work toward reaching their investment goals. He is the recipient of the 2007 Malcolm S. Forbes Public Awareness Award for Excellence in Advancing Financial Understanding.

“On my 41st anniversary in our great profession, I did a piece for Financial Advisor magazine called “Forty-One Epiphanies,” listing that number of great realizations I'd experienced during those years. Below is an excerpt of the 20 epiphanies that are client-oriented." ―Nick Murray

1. Most people who invest most of their capital in fixed income investments as they go into retirement will run out of money well within their lifetimes, and will die destitute and dependent upon their children. Equities = life. Bonds = death-in-life.2. Optimism is the only realism. It is the only worldview that squares with the facts and with the historical record.3. Get a year's living expenses in a money market fund as quickly as you can, even if you have to live on coffee and rice while you're saving toward this goal.4. The origin of all wealth is threefold: personal initiative, hard work, and thrift. Tell me the percentage of your income that you're putting away, and I'll tell you whether you're going to achieve your financial goals.5. The world does not end. It only seems to be ending. This time is never different.6. Americans say they want safety and income. What they really want is all the income they can get, and the illusion of safety. More money has been lost in the quest for the chimerical combination of safety and high yield than in all the stock market crashes in history.7. The only sane investment objective in retirement is an income that grows at a minimum of the same rate at which one's cost of living is rising.8. Disciplined diversification is a pact with heaven: I will never own enough of any one thing to be able to make a killing in it; I will never own enough of any one thing to be able to be killed by it.9. All investment “new eras” end in ruin, because all inventions follow the same arc, from miracle to commodity.10. Price and value are inversely correlated. When the price of any investment sector is rising, its value is declining; the converse is also true.11. The most fascinating aspect of all financial crises is their essential sameness.12. Get out of debt, and stay out of debt. Keep your nut as low as you possibly can, especially in “good times.”13. What goes around comes around, even if it's on a very long, elliptical orbit.14. Inflation is always and everywhere a monetary phenomenon.15. The advance is permanent. The declines are temporary. There have been thirteen bear markets with an average decline of 30% since the end of World War II. The first one started on May 29, 1946. That day, the S&P Index closed at 19.5 As I write, thirteen ends-of-the-world later, it is 1,575. Stocks are up nearly eighty times over these seven decades because earnings are up nearly eighty times.16. The dominant determinant of the real long-term returns real people really get isn't investment performance. It's investor behavior.17. Protectionism always raises consumer prices above where they would otherwise be; it also invariably destroys more jobs than it “saves.”18. All investments are income investments. They are made for the production either of current income, or of future income, or of income for someone else. The only sane test of an investment's long-term income-producing potential is its long-term total return, not its current yield. By that one sane test, equities are a far better income investment than bonds.19. The computer in your cell phone is a million times smaller, a million times cheaper, and a thousand times more powerful than the mainframe computer used by E.F. Hutton & Company on the day I joined that firm, May 1, 1967. This is a billionfold increase in computing power per dollar. In the next quarter century, there will be another such billionfold increase, at which point technology will have essentially solved all our current problems: energy, the environment, poverty and disease. This is the exact worst moment in human history to turn pessimistic.20. Ten thousand people a day are retiring in this country every day, without a clue that their basic financial challenge is not loss of principal but erosion of purchasing power.

In addition to his lessons above you should also read some of his best quotes and musings.

With over three decades in the Investment Advising business, I can attest that this is the simplest and most effective investment book I’ve ever read.If this book resonates with you, then you’ll enjoy working with me. If it doesn’t, you won’t.

Invest in Real Estate or the World's Great Companies?

A question I get occasionally is, "What about investing in real estate?" It's a valid question so let's compare real estate to investing in a broadly-diversified collection of the world's great, publicly-traded companies.

“Real estate is a business, not a passive investment." ―Dave McDanal

Performance

Which generates a greater return on investment: stock ownership of Google, Exxon Mobil, Coca-Cola and JP Morgan Chase, or the buildings they occupy?The absolute silliest of all real estate illusions is that one's home (or rental property) provides significant growth of capital. Since 1945, according to the Nobel laureate Robert Shiller, American family home prices have risen at a rate of about 4% per year.Whereas the return of the American Funds Investment Company of America since 1945 has been 12%. And you don't have to heat the the ICA in the winter.

“Someone who claims to think that buying an apartment complex or an office building or a strip mall ― or all three ― will produce a greater return on his capital than does owning a basket of the 500 largest, most profitable, most soundly financed and most innovative companies in America and the world is not rational." ―Nick Murray

Security / Safety

Most people invest in real estate because they don't understand equity mutual funds or think they're "risky". They believe that real estate is a safer investment than equities.But are they really?If you own and are liable for the mortgages of those four companies’ buildings mentioned above, your position inherently carries much greater risk than if you owned the stocks, where there is no personal liability. (That, among other things, is actually the genius of common stocks, and indeed of the corporate form of organization.)There is also one overwhelming benefit of mutual funds, which is of course diversification (as an example, the American Funds Growth Portfolio invests in over 1,200 companies from all over the world). If you end up, late in life, with the huge preponderance of your net worth in essentially the same leveraged, illiquid asset class, it won’t matter what the relative risks of equities and real estate are perceived to be: you will have raised your own personal risk profile to and beyond the red line.

Maintenance, Costs & Flexibility

Real estate is inherently illiquid, incurs substantial acquisition and disposition costs, and demands significant management oversight. It is subject to recurring expenses, such as property taxes, homeowners association fees, and maintenance costs, which are paid separately.In contrast, mutual funds present a more streamlined investment proposition. They incur a one-time cost (which is waived for investments exceeding $1M), and have very low annual expenses which are deducted directly from the account (usually less than 0.8%). Note: you can also purchase mutual funds as C-shares or F-shares that don't have an upfront charge, however the annual expense (which lasts forever) is much higher, often double.Mutual funds are very flexible in their withdrawal allowances. Should you wish to take out a portion of your investment, this can be easily accomplished online or with a phone call, and must be completed within a maximum of five business days, by law. Conversely, real estate does not offer this flexibility, as partial withdrawals are not feasible (if you need $20,000, you can't just sell your garage!).Moreover, real estate income is fixed, regardless of your immediate needs. For instance, if a rental property generates $1,000 per month, but you require only $800, the excess $200 cannot be 'left' in the property. Mutual funds, however, allow for such flexibility, as you can withdraw only the amount needed, leaving the remainder to compound for future growth.Finally, mutual funds can be paired with a variable annuity (don't use "fixed" or "index" annuities!) in order to generate a guaranteed monthly income for life (on two spouses), while the balance continues to be invested in the world's great companies. This guaranteed income will increase when/if the mutual funds grow, but never down. When both spouses die, the children inherit the balance of the account. This guaranteed lifetime income is not possible with real estate.

I'll leave you with this article by Nick Murray...

Investor vs Investment Performance

“The best investors in the world are really good at doing nothing for long periods of time." ―Michael“The investor is more important than the investment." ―Dick Fabian

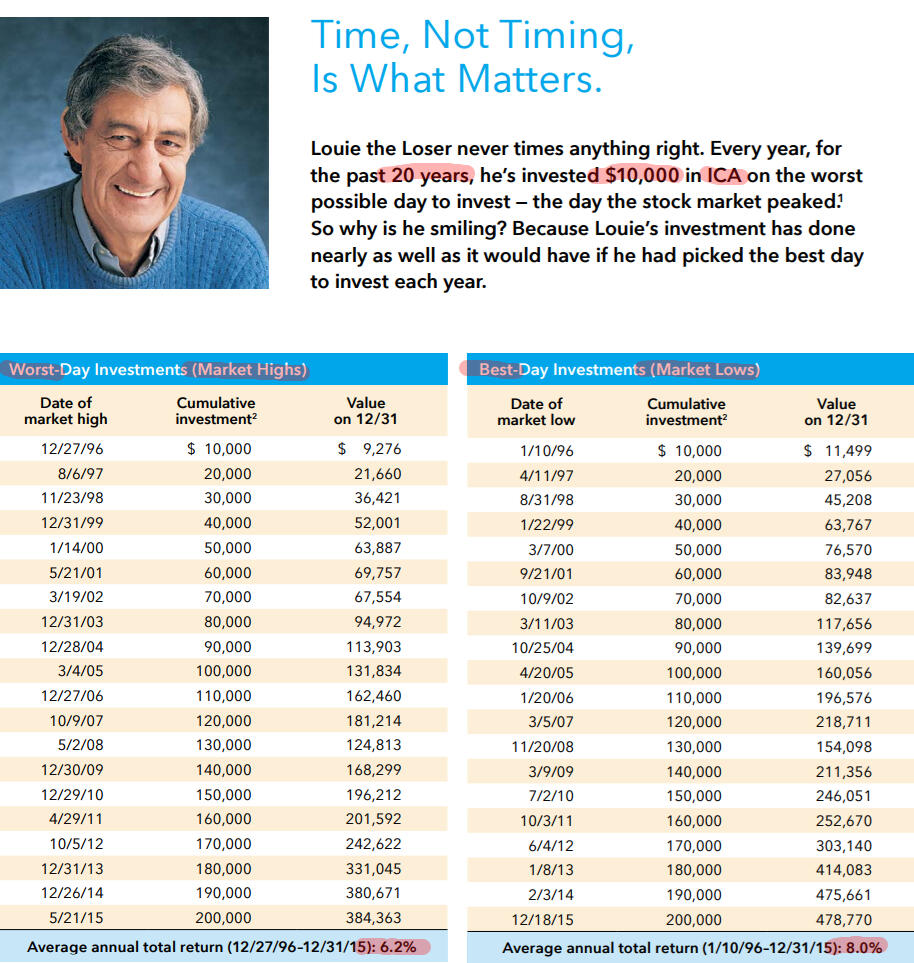

How Can The Driver Be Slower Than The Car He's Driving In?

If you compare the average speed of a driver in a car to the average speed of the car, how would it be possible that the two are different?Here's how: a car traveling on a specific route usually moves at a rate of 60 mph, but our particular driver frequently takes breaks or second-guesses the pre-planned route and takes detours; thus his average speed is less than 60 mph.Investors do the same thing: they invest in a mutual fund that averages ~12% over all ten year periods (such as the American Funds ICA), yet they only get a 10-year return of 6% because instead of investing and leaving it alone, they pull their money out when the market drops and re-investment when market is up (selling cheap and buying expensive).Then they blame "the market", the mutual fund and even their Advisor. The driver is blaming the car or the pre-planned route instead of himself.

“Investing is easy, it's clients that get in the way" ―Michael

Take a look at the chart below which shows the average rate-of-return over twenty years of the driver (investor) vs the car (the investment).

(Source: Capital Group Literature number INGEFL-050-0522)

In my 35+ years of coaching clients, I've found the differences between the two to be much more pronounced, especially over longer time-frames. Most investors without a coach aren’t disciplined enough to stay on track (ie, staying in the market when it's down).

Why Do They Do This?

Why do investors "get out of the car" or go off of the planned route?Fear and Greed.Driven by these emotions, clients often engage in such negative behaviors as chasing the hot manager or asset class, avoiding areas of the market that were out of favor, attempting to time the market, or otherwise abandoning their investment plan.

"If you cannot control your emotions, you cannot control your money." ―Warren Buffett

During periods of uncertainty, investors often gravitate to the investment media for insights into how to position their portfolios. While these forecasters and prognosticators may be compelling, they usually add no real value.

"Don’t try to time the market. It’s very, very difficult to do. There may be a couple of people in the world who can do it, but if there are, they’re not telling you." ―Ben Bernanke

The Wall Street Journal Survey of Economists from December 1982 – December 2010, showed that economists’ forecasts were wrong in 37 of the 57 time periods – 65% of the time!Every public trade that's ever been transacted since the 1800's is logged in a computer(s) somewhere, and if by now a pattern to the market hasn't been discovered, it isn't going to be.

“The sole function of economic forecasting is to make astrology look respectable. There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.” ―John Kenneth Galbraith

Do not waste time and energy focusing on variables that are unknowable and uncontrollable over the short term, like the direction of interest rates or the level of the stock market. Instead, focus your energy on things that you can control, like creating a properly diversified portfolio and staying in it!My best clients have understood that building long-term wealth requires the ability to control one’s emotions and avoid self-destructive investor behavior (with my help).

Even If You Could Time the Market, It Doesn't Make Much of a Difference

The Solution: Do Nothing (Buy and Hold)

“Don't watch the market closely. Buy and hold is the best strategy. The money is made in investments by investing, and by owning good companies for long periods of time.” ―Warren Buffett

Stop watching and obsessing over the market! Doing nothing is often the best investment strategy. Let the market do what it is supposed to do. You can't control it anyway, so don't try!

"When the spaghetti hits the fan, don't just do something: stand there. This too shall pass. You see, what happens in the equity market has very little to do with what actually happens to the equity investor. That's because the dominant determinant of long-term, real-life outcomes is not the performance of markets but the behavior of investors." ―Nick Murray

We can only control our participation in the market, and our behavior while we’re in it.

"Fidelity has done a study as to which clients had done the best at Fidelity. They were the people who forgot they had an account!" ―James O'Shaughnessy“Investing is like a bar of soap… The more you touch it, the smaller it gets.” ―Darcy Howe“If you spend more than 13 minutes analyzing economic and market forecasts, you’ve wasted 10 minutes.” ―Peter Lynch"Personal finance is 80% behavior and only 20% head knowledge." ―Dave Ramsey

The Antidote: A Professional Advisor

“At the end of an investor’s life, less than 5% of his total lifetime return will come from what his investments did versus other, similar investments. The other 95% will come from how the investor behaved. And the primary determinant of that behavior will be the quality of the advice he got, or didn’t get.” ―Nick Murray

I am a long-term advisor serving clients with long-term goals. If a client is exhibiting short-term behavior or emotionally reacting to short-term market conditions, I need to have a serious discussion with him about his goals, and reassure him that a long-term perspective is the best perspective. My greatest value to my clients is my ability to influence their behavior in a positive way.

“The investor needs a confident, seasoned professional keeping him on the right track... making sure he stays diversified and insulated from his own tendencies toward greed and fear.” ―Nick Murray from his book Serious Money“People make better decisions with financial advisors.” ―Robert Shiller, Nobel Prize-winning economist“Without an adequately compensated advisor to help with selection and discipline, the individual investor will simply make all the classic and horrendous mistakes.” ―Nick Murray“Proper investment strategy is as much of a psychological as an intellectual challenge. It is often best to seek professional help to structure and maintain a well-diversified portfolio.” ―Jeremy Siegel

To see how I implement this philosophy with my clients read WHAT I DO AND WHAT I DON'T DO.

The Magic of Compound Interest

“Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it..” ―Albert Einstein

The Power of Compounding

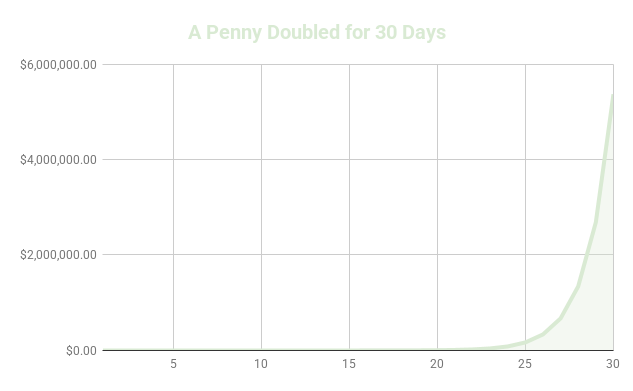

Let's look at the incredible power of compounding. An old question that beautifully illustrates this is:Would you rather have $1,000,000 or a penny that is doubled every day for 30 days?

Doubling a penny 30 times = $5,368,709! (It actually only take 28 days to surpass $1M.)

What Is Compound Interest?

I used to think that the interest rate on an investment was pretty simple — you invest your money at 5% and get “X” in return. Then if your investment returned 10%, it would be “X” times two. Right?WRONG. That's when over 35 years ago someone showed me a compound interest table and explained the magic of compound interest, which is one of the most amazing facets of financial management.Compound interest is the interest calculated on the initial principal and also on the accumulated interest of previous periods. This means that interest is earned on both the initial amount and the interest that has been added to it over time.For example:1. If you deposit $100 at a 5% annual interest rate, at the end of the first year, you would have $105.

2. In the second year, you would earn 5% on $105 (not $100), resulting in $110.25.

3. This process of earning interest on interest occurs year after year and leads to exponential growth.Again, doubling the rate-of-return doesn't simple double the result. Look at the example below of fully-funding two IRAs for a married couple ($7,000 per person, per year):

12% earns three times as much as 6%. Amazing, isn't it?

“I don’t know what the seven wonders of the world are, but I know the eighth, compound interest.” ―Baron Rothschild

How It Works ― The Rule of 72

The simplest way to understand of compound interest is the Rule of 72. It is a simplified formula that estimates the number of years it will take to double your investment.

The math behind it works because doubling is linked to how percentages compound over time. The exact calculation involves logarithms, which are used in higher-level math to solve problems related to exponential growth. But the Rule of 72 skips all the complicated calculations by relying on a close approximation that works well for most realistic growth rates.It’s not perfect — its accuracy wobbles with very high or very low interest rates — but for rates between 4% and 15%, it’s remarkably accurate. Economists trace its origins to 15th-century merchants who marveled at the power of compounding long before financial calculators existed.The correct rule should be:69.3 / Interest Rate = Years to Double MoneyBut we use 72 instead of 69.3 because it has a lot of divisors so it can be easier to do mentally. For example, 72 divides cleanly into 1, 2, 3, 4, 6, 8, 9 and 12, allowing for a quick and simple division problem instead of using a compound interest calculator.

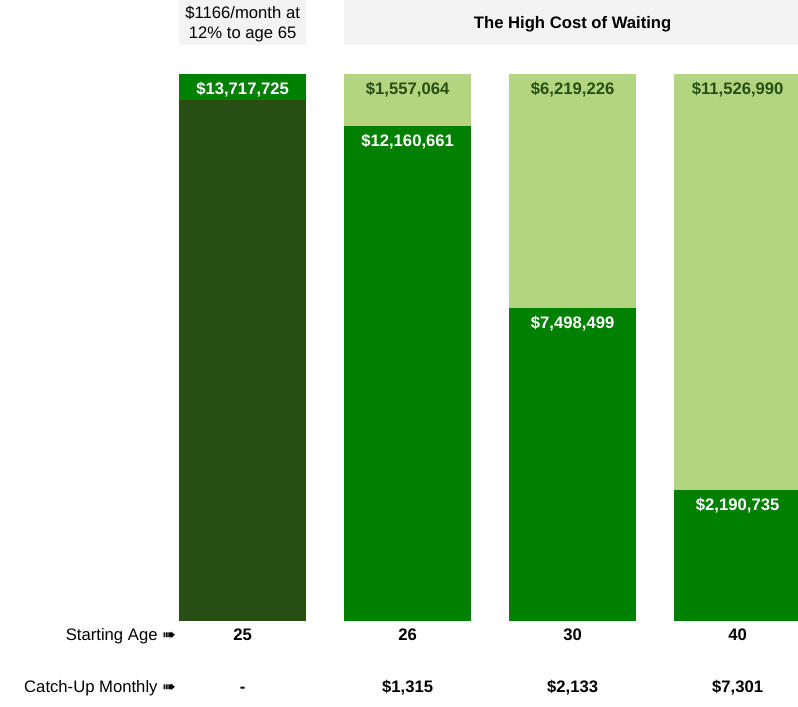

The High Cost of Waiting

"Never interrupt the compounding." ―Charlie Munger

The power of compound interest is amplified by time ― the longer you keep it going, the more your money grows. But the reverse is also true.Let's look at two examples of waiting to invest and thus robbing you of compounding.Example 1: Delaying One Year Costs You $1.5M

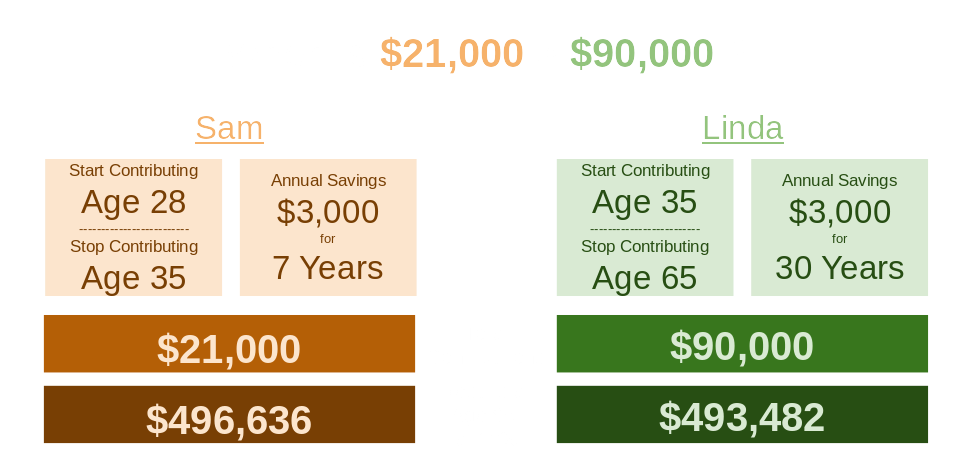

In the above chart, we notice the following:1. Fully-funding two IRAs for a married couple from age 25 to 65 (40 years of saving) and earning an average of 12% rate-of-return, will build them a $13M nest-egg.2. By waiting just one year to start their IRAs (39 years of saving) it costs them $1.5M!3. By waiting five years to start their IRAs (35 years of saving) it costs them $6.2M!4. By waiting 15 years to start their IRAs (25 years of saving) it costs them $11.5M!At the bottom of chart you can see the amount of extra monthly contributions it would take to catch-up to the original value. Scary.Example 2: When is $21k > $90k?

Let's compare Sam and Linda, two 28-year-olds contemplating saving for retirement in a long-term equity mutual fund earning an average of 10%:1. Sam begin investing immediately and saves $500 per month for seven years. Then he stops contributing due to family and other financial obligations. However, he doesn't withdraw any money and lets it compound until age 65 and ends-up with $496,636.2. Linda, due to not having extra cash, decided to delay investing for seven years until she is 35. However, once she starts contributing she doesn't stop and continues until she is 65. She ends-up with $493,482.Sam contributed $21,000 and accumulated $496,636. Linda contributed $90,000 and accumulated $493,482.This demonstrates both the power of starting early, and the high cost of waiting.

“Compound interest is ugly in the early years, but beautiful in the later years.” ―Michael

Even the smallest amount of money, saved systematically over a period of time (Dollar-Cost Averaging), will multiply far beyond your expectations through the magic of compound interest. No amount is too small or insignificant to save. The important thing is to get some money started working for you as soon as possible.

“If you understand the math behind compounding you realize the most important question is not ‘How can I earn the highest returns?’ It’s ‘What are the best returns I can sustain for the longest period of time?’” ―Morgan Housel

What The Experts Say About Using Variable Annuities For A Guaranteed Income

When you’re approximately 10-years from retirement withdrawals start considering a variable annuity with a guaranteed income rider. This will provide a minimum 5% guaranteed withdrawal for the rest of your life, while staying 100% invested in the world's great companies, (and you only pay taxes on the withdrawals while the balance remains tax deferred). When you pass away, the income continues guaranteed for your spouse. When he/she passes your children inherit the account balance.Note: this section is not a detailed explanation on how this works, but mostly a collection of quotes from the experts in the field.Start by reading what American Funds says about variable annuities.

"I know of only two ways of coping with equity volatility during retirement withdrawals:1. Abiding faith in the historical record, in the greatness of free-market democratic capitalism.2. The other method is what the variable annuity industry is pleased to call 'living benefits'.”―Nick Murray, On Panic, Faith, and the Determined Primitive

"Insurance companies promise that annuitants won't run out of income, ever! When there is a living benefit, an annuitant may run out of cash but not out of income.” ―Richard Hoe, ChFC, CLU, AEP. From the article "The Better IRA" in The Investment Edge magazine.

From the Article: Annuities Are Coming in New Shapes and Sizes

Barron's article, July 28, 2025...once you’re retired, by establishing a reliable lifetime income stream to supplement Social Security.The major stock market dip in early April underscored a major benefit of annuities’ income guarantees: peace of mind. “We had to talk a lot of people out of pulling money out of the market,” says Howard Sharfman, at NFP Insurance Solutions. “But nobody who has guaranteed income called us to have that discussion.”There are other benefits, too. “You can take more risk by holding more in stocks because you have the income in place with the annuity,” Elder says. “You don’t need to provision as much money for later in life because you know you have an income floor. So you can use the money earlier.”Variable annuity is the best choice because it doesn’t cap upside and allows you to potentially build more assets.

Moshe Arye Milesky is a tenured professor at York University. He has a Ph.D. in Finance, a Master of Arts in Mathematics and cum laude from Yeshiva University. He is a lifetime Fellow of the Fields Institute for Research in Mathematical Sciences. Over the last 25 years he has published 15 books and 60 peer-reviewed scholarly articles on wealth and risk management. He currently serves as a member of the editorial boards for the Journal of Pension Economics and Finance (JPEF), and Insurance: Mathematics and Economics (IME).

“I purchased a variable annuity with a guaranteed living benefit and allocated 100% to stocks.” ―End Notes from the book In Defense of Annuities (2021).

“... with a guaranteed and predictable lifetime of income that can't be outlived.” ―Section IV from the book In Defense of Annuities (2021).

“A living benefit is paid to the annuitant for as long as they live and ceases upon death.” ― Section V from the book In Defense of Annuities (2021).

“It protects against the risk of living beyond, even far beyond, life expectancy - without surrendering either upside potential of liquidity of the underlying portfolio.” ―Section V from the book In Defense of Annuities (2021).

“The income is guaranteed to never decline for the remaining life of the annuitant. If the underlying investment portfolio ever reaches zero, the guaranteed income will continue so long as the annuitant or, for a joint product, one member of the couple is still alive. Whatever remains in the account at the time of death goes to the heirs.” ―Section V from the book In Defense of Annuities (2021).

“... to provide an assortment of lifetime income guarantees meant to protect the policyholder against longevity risk as well as what the industry has coined as ‘sequence-of-returns risk’, which refers to the chance that a retirement portfolio, from which cash is being withdrawn, suffers early losses, magnified by the retiree living longer than average. All you need is a bear market at the wrong time, and the sustainability of your income can be cut dramatically.” ―Section V from the book In Defense of Annuities (2021).

“By promising a lifetime of retirement income, insurance companies are taking on the above-noted longevity risk.” ―[Section V from the book In Defense of Annuities (2021).

“Invest aggressively, diversify, exposure to equities, and wrap some protection around it. Optimize your variable annuity by having an aggressive allocation and protecting it with a lifetime income.” ―From his Annuities for a Biological Age webinar (2020).

“Fees and periodic withdrawals are deducted from the VA account as long as there are funds available. But if those periodic withdrawals every fully deplete this account, the insurance component is triggered to fulfill the remaining withdrawals for the lifetime of the investor.” ―Section V from the book In Defense of Annuities (2021).

John Huggard, J.D., CFP, CLU, ChFC, is a sought after expert witness in securities cases and a nationally recognized speaker on the topic of variable annuities.

“Win-Win Situation:

- If the market goes up - you're a winner.

- If the market goes down - you're a winner.

- No more disgruntled clients.―Page 42 from his lecture notes, "Understanding the New Variable Annuity Living Benefit Riders" (January 8, 2007).

“Living Benefits are not new variable annuities, but riders available with existing variable annuities. Often, only a box on the application need be checked to obtain a specific living benefit. Living benefit riders provide long-term investors with:

- An opportunity to obtain stock market gains if the market goes up.

- An opportunity to obtain an upward ratcheting lifetime stream of income regardless of the stock market's future direction without annuitization.

- The ability to avoid the 'longevity problem' for both spouses.

- The ability to avoid the 'sequence of return' trap.

- The advantages of obtaining basic variable annuity benefits (commission-free investing, no transaction costs, death benefit, etc.).”―Page 8 from his lecture notes, "Understanding the New Variable Annuity Living Benefit Riders" (January 8, 2007).

Re-Balancing: A Free Lunch In Portfolio Management

If an investment is successful, naturally, you'd want to stick with it. The last thing you'd want to do is sell some of your winners to invest more money in your investments that aren't doing as well. Right?Well, no.Unfortunately, human nature’s default investment policy is: let’s sell whatever has performed most poorly over the last block of time so we can buy more of whatever has gone up the most (selling when it's down and buying when it's expensive). We intuitively chase immediate past stellar investment performance, which is not, to put it charitably, an optimal long-term strategy.One of the most powerful and practical antidotes to this counterproductive impulse is: re-balancing.

What is Re-balancing?

“Re-balancing means always shopping the sales, automatically.” ―Nick Murray

Re-balancing is an essential part of managing your investment portfolio by trimming back on winners allowing you to buy more of a laggard, protect your gains, and position your portfolio to benefit from the next uptick in the market. Basically, you are always selling high and buying low.Suppose your mutual funds are allocated equally among three distinctly different equity sectors: large-company (33%), small-company (33%), and international (34%).Over the course of a year or two, let’s say, the three sectors will very likely have appreciated differently to a point where they now each represent more or less than the original 33% of your overall portfolio.The plan is to re-balance the three sectors back to their original percentages. Which means that you will sell off enough of the over-performers to reduce them back down to 33% of the portfolio — and reinvest the proceeds to bring the laggards back up to 33% each.This rational discipline is the direct opposite of the most basic human instinct.

“Re-balancing is there to save us from ourselves.” ―Nick Murray

Re-balancing causes you regularly to be lightening up on sectors that have become relatively expensive (and thereby potentially more fully valued, if not overvalued) in order to increase your positions in those that have become relatively cheaper (and therefore potentially more attractively priced, as the current market shuns them).Re-balancing creates a systematic way to buy low and sell high.

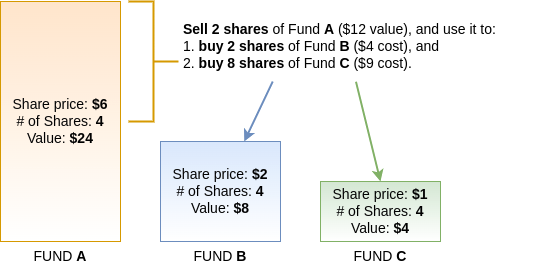

An Example

“We sell high for the express purpose of buying low.” ―Nick Murray

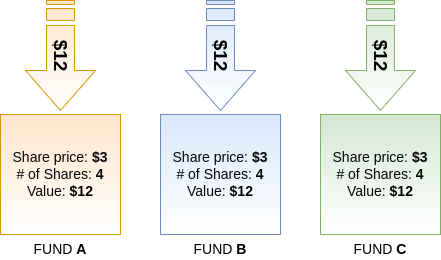

Step 1: Invest $36 into Three Mutual Funds, Equally

- Total shares: 12

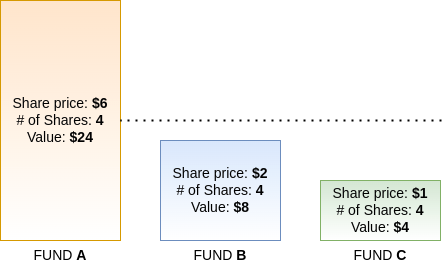

- Value: $36Step 2: Six Months Later... They're Out of Balance- Fund A grew more than Funds B and C.

- Fund B decreased some.

- Fund C decreased the most.

- Total shares: 12 (no change)

- Value: $36 (no change)Step 3: Re-balance- So, let's re-balance by selling 2 shares of Fund A and use the proceeds to buy more shares of Fund B and Fund C.

Step 4: After Re-balancing

By rebalancing your portfolio, you have increased your number of shares from 12 to 20 without adding new money!If this is done within a tax-advantaged account, such as a 401k, IRA or variable annuity then there are no tax consequences.- Total shares: 20 (you increased your shares without adding an money!)

- Value: $36

“Re-balancing, much like dollar-cost averaging itself, is smarter than we are.” ―Nick Murray

The Benefit

“An annually re-balanced portfolio will outperform the same portfolio without re-balancing.” ―Nick Murray

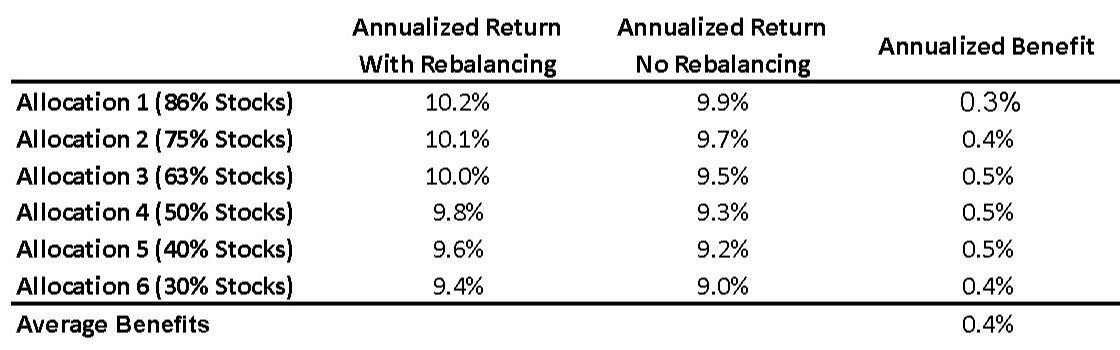

If you re-balance regularly, it is possible to add an extra 0.3% - 0.5% on top of your returns over the long haul. Generally, the more frequent the re-balancing, the better.Example: for the years 1968-1991:

If re-balancing within a tax-shelter (IRAs, 401ks, Variable Annuities) then there are no tax-consequences of trading shares, and many firms have automatic re-balancing programs at no extra cost.

Three Rules of Re-balancing

1. Only re-balance non-taxable accounts (ie, qualified accounts and variable annuities). Unless it is built-into the investment, such as the American Funds Growth Portfolio (one of my favorites).2. Re-balance as often as possible. Example: American Funds allows quarterly, and Jackson variable annuities allows monthly re-balancing.3. It's best to set-up automatic re-balancing. But if you insist on doing so manually, then do so the same day regardless of the market. Don't turn re-balancing into market timing.

“The most effective tool for overcoming the very human performance-chasing impulse is rebalancing — the act of systematically selling off pieces of overperforming sectors annually re-balanced portfolio will outperform the same portfolio without re-balancing.” ―Nick Murray

Why Not Invest in Gold?

This question usually comes from people with one of two philosophies:1. They think Armageddon is imminent and only gold is "safe"; or2. They actually think it is a good investment.

To overcome the first belief is more difficult as it requires a shift in fundamental philosophy. If you don't believe that the world will continue as it always has, and you don't have faith in the future, there is nothing further I can say to persuade you otherwise. By the way, if civilization truly does end, gold won't help either - no one is going want colored rock, they want canned food and water.The second belief is what we will address today - whether gold is a good investment or not. And if not, what is a better alternative.

“Gold is colored rock which has no intrinsic value. Its value is arbitrary and derived from speculation ― whatever someone else is willing to buy, or sell it, for.” ―Michael

The Persistent Illusion of Gold

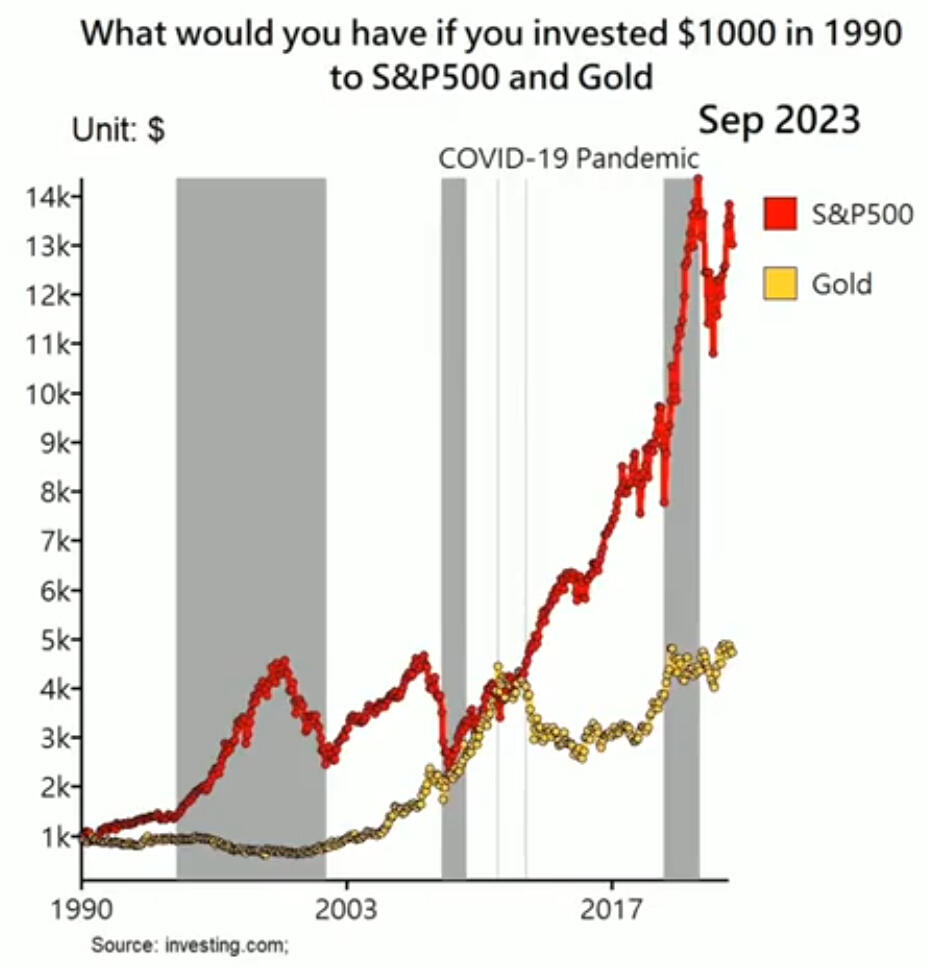

The August 7, 2023 online edition of the Wall Street Journal contained a remarkable article titled “When Markets Get Scary, Mom and Pop Buy Gold.” In addition to being a fair sample of everything that’s wrong with financial journalism, it’s a common recitation of the perceived benefits of owning gold.The statistic at the heart of the article is as follows:

“The percentage of Americans who believe gold is the best long-term investment jumped to 26% this year from 15% in 2022, according to a Gallup report from May. In contrast, those preferring stocks dropped to 18% from 24% last year, while those favoring bonds climbed to 7% from 4%.”

The illusion is not just that gold is an efficient inflation hedge but that it is somehow preferable to holding a broadly diversified portfolio of quality common stocks (ie, mutual funds) for the long term.First, let’s get our terminology straight: gold is not an investment at all. That is, it does not produce anything. It just sits there. In fact, it costs money to store and to insure.If you bought an ounce of gold nearly 44 years ago at $800, you now own an ounce of gold worth (as of Sep 2023) $1,965. It’s up about two and a half times, having produced neither dividends, nor interest, nor anything else. The Consumer Price Index in January 1980 stood at 78. In July of 2023 it was 306. It’s up just shy of four times. Which means that, just to have kept up with inflation, your $800 gold ounce would now have to be valued pretty close to $3,200. But it isn’t. Not even close.Wait, it gets worse. The Standard & Poor’s 500 Stock Index at the end of January 1980 stood at 115. As of Sep 2023 it sits at 4,490. That’s right: while the price of gold was rising two and a half times, the S&P 500 went up 39 times, not counting dividends which — at the risk of repeating oneself — gold does not pay.

“Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again, and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.” ―Warren Buffett

A Better Option: The Great Companies of the World

Ultimately, gold has money-market type returns with the volatility of the S&P 500.

“You could take all the gold that’s ever been mined, and it would fill a cube 67 feet in each direction. For what that’s worth at current gold prices, you could buy all, not some, of the farmland in the United States. Plus, you could buy 10 Exxon Mobils, plus have $1 trillion of walking-around money. Or you could have a big cube of metal. Which would you take? Which is going to produce more value?” ―Warren Buffett

“While businesses were reinvesting in more plants and new inventions came along, you would look into your safe deposit box, and you'd have your 300 ounces of gold. But it didn't produce anything. It was never going to produce anything.” ―Warren Buffett

If you insist on investing in gold, I recommend finding a mutual fund that invests in companies that deal with gold, but never directly in gold itself.Ponder this: if gold is such a great investment and these gold-selling companies you see on TV are telling you it's is going to increase so much in value - why in the world would they sell it to you?! Wouldn't they just hold onto this "great investment" for themselves?https://clientfirst.pro/#equities

“The only two things that actually make money are printing presses and the great companies of the world ― and the first is illegal.” ―Michael

What the Experts Say about American Funds

American Funds is my investment manager of choice (they manage all of my family's money). As an independent Advisor I have access to every mutual fund family in America, but I have been exclusively recommending AMF for over two decades (with rare exceptions).I will not dive directly into the inner workings of AMF but instead quote what others have stated about the firm.

"For the entirety of my half-century career, no mutual fund company has ever championed long-term equity investing as consistently, eloquently and even relentlessly as have the American Funds. Indeed, there's been nobody close; the American Funds group has been in a class by itself. I have always applauded them for this unreservedly." ―Nick Murray

"Welcome to what many believe to be the world’s best fund management organization." ―Financial Times

"American Funds sells mutual funds you could bring home to meet your parents: the funds are described with words like steady, solid, and dependable" ―Boston Globe, September, 17 2004

"The American Funds family of mutual funds is one of the largest of its kind in the world because investors and advisers alike are attracted to the low-cost, high-quality attributes that combine for the best funds to buy. You’ll especially find American funds in retirement accounts like IRAs and 401(k)s because their portfolio managers’ long-term outlook and dozens of years of experience result in portfolios that are built to last."

"Therefore American mutual funds don’t often hit the lists of best short-term performers — they are typically among the best performers for long-term periods, such as over five and 10 years and beyond." ―InvestorChoice, December 2015

"They have funds that have consistently outperformed and consistently been lower-cost versus their active peers." ―Todd Rosenbluth, director of ETF and mutual-fund research at CFRA

“American Funds very visibly accomplishes what index-fund proponents claim cannot be done: outperform year after year, decade after decade.” ―Morningstar, January 30, 2014

"A long-term broadly diversified collection of the world's great publicly-traded, mainstream companies (ie, mutual fund), is the finest, most transparent, simplest, low-stress and most effective of any investment in the history of humankind. And American Funds is the best at it." ―Michael

"The American Funds group has won a legion of admirers for its distinctive investment approach... ‘We like their management and their people,’ says a marketer for one of the fund’s biggest distributors. ‘We like their buy-and-hold philosophy. They don’t surprise us.... They’re defensively managed." ―Barron’s, January 12, 2004

"The American Funds line-up follows an ‘old-school’ approach that is coming back into favor, said an analyst at Morningstar.... ‘They buy for the long-term because they like the business....’ There is also an emphasis on dividend-paying stocks, which is timely because of tax breaks which took effect last year. American Funds wins fans with conservative style." ―Reuters News, January 9, 2004

"American Funds has a strong record of acting in shareholders’ interests, by keeping costs low and focusing on long-term results.... We think that their funds... remain attractive options." ―Morningstar Mutual Funds, January 6, 2004

"American Funds has focused more on retaining the top investment talent... than on gimmicks such as rolling out new funds." ―Morningstar Fund Family Reports: American Funds, December 2003

"As for why they’re steering their clients toward American Funds, advisers mainly say it’s their consistent performance and low annual cost — qualities that seem to engender a considerable level of trust." ―Dow Jones News Service, October 13, 2003

“American Funds gives you Nordstrom service with Tesla performance at Walmart prices.” ―Michael

This book lays out the incredible history of Capital Group. Find out what makes American Funds so special.

"Capital (American Funds) is the best managed investment organization… that I’ve known as a consultant over the past 40 years. I’m confident that Capital is one of the best and quite likely the best designed, best staffed, and one of the best managed professional firms in the world." ―Charles Ellis, author of "Capital""Capital, the parent firm of American Funds, is one of the finest business organizations in American Business. This book was written by an index fund /no-load proponent who was looking to debunk American Funds (which are neither indexed, nor no-load) and instead he (Ellis) discovered their exceptional values, performance and pricing. This story is fast-paced and highly interesting, both to Advisors and clients." ―from the forward of the book.

What Capital Group / American Funds Says...

In this 23-minute video (2024-06), Mike Gitlin, CEO of Capital Group, joins David Rubenstein on Bloomberg Wealth. At a minimum, watch the first 12 minutes and the last 5.

“There are 290,000 financial advisors in America. 212,000 of those own a Capital Group strategy for their clients.”“For 94 years ― it's not just about the destination but about the journey. And our clients like a calm journey. Don't reach for the last basis point of return or yield - but think about how the client is experiencing the journey and they''ll always appreciate that you took them on a smoother one rather than a rougher one.” ―Mike Gitlin, President and CEO of Capital Group

“We have this 'Capital System' (at Capital Group / American Funds) where money managers are encouraged to have their own points of view and to express it. Trying to understand management teams (of companies to invest in) and their quality is huge for what we do. And, in fact, is one of our most important strategic advantages. The index funds don't spend any time evaluating management, not one bit. If we can do that well, that really gives us an advantage.” ―Don O'Neal, Capital Group Portfolio Manager

Their Three Most Important Values

I don't want to go too much down a rabbit hole of statistics but I do want to mention three of their values that are aligned with mine (and Nick Murray's), and thus make them a wonderful solution for our investment philosophy.1. The Capital System is distinctive way of managing moneyEarly in Capital Group's history, they realized that their funds would outlast the professionals who managed them. So they asked themselves a key question: If a portfolio manager left the firm, how could they keep funds going strong?Answer: By dividing funds into sections and giving each of the existing managers a portion to administer, no fund would be too dependent on a single person.

“By incorporating the highest conviction investment ideas of each manager in a fund, we aim to both increase the diversity of those ideas and reduce the volatility of a fund, which can give you a smoother ride in bumpy markets.”

2. They take a long-term approachTheir investment managers’ compensation is tied to short-, medium- and long-term results, with a greater focus on the long term. Also, Capital Group is a privately held firm, so rather than being distracted by what’s good for "the Street," they can focus on what’s best for long-term investors.

“We invest in companies for the long-term, not buy stocks for the short-term.” ―this was told to me personally by one of their fund managers.

3. Their deep and fundamental research is the backbone to delivering superior results.They believe that the best way to get to know a company is to know the people behind the business. they get to know both upper management and the employees on the ground.

“Meetings are essential to our research. Our investment professionals conducted more than 20,000 meetings with companies in 2023.”

This is my favorite investing podcast from my favorite management company.Want to learn how professional investors do it? The weekly, 30-minute Capital Ideas / American Funds audio podcast brings you the latest investment thinking from Capital Group. Each episode gets inside the minds of portfolio managers, analysts and economists to break down market trends, macroeconomic forces, investing approaches and lessons learned from personal experience.

Capital Conversations is a Capital Ideas video podcast offering an unscripted look into The Capital System.Join Mike Gitlin (CEO of Capital Group) as he hosts in-depth discussions with Capital Group's portfolio managers, analysts and senior leaders from around the globe. Gain unique perspectives on investment strategies and market trends while getting to know the people behind the portfolios.

Where and How to Invest for Long-Term Growth?

A successful investor needs three things: :1. The Right Plan.2. The Right Investment. (This is what we'll discuss today).3, The Right Coach. (Hopefully you'll agree that that's me!)

I've previously written about the power of Compound Interest and the dramatic effect it can have on your long-term investing. But, you may ask, how and where is the best place to invest in order to take advantage of this magic?1. Publicly-traded companies are the best long-term investment.2. Equity mutual funds are the best method of investing in publicly-traded companies.

U.S. Publicly-Traded Companies Since 1926

1. Inflation = 3%. Bonds = 6%. Large U.S Companies = 10%. Small U.S companies = 12%.2. In the ninety-nine 12-month rolling-periods the market's return has been positive 74% of the time. Specifically, annual returns have been positive 73 times and negative only 26 out of 99.3. However, the market very rarely returns anything close to 10% in any given year. In the 99 years 1926 through 2024, the market has come within two percentage points of 10% only seven times. The best year returned 54%, and the worst year was down -43%.4. Declines of -5% occur about three times a year.5. Declines of -10% occur about once a year.6. Declines of -15% occur about once every three years.7. Declines of -30% occur about once every five years (Bear Market).8. 40 months is the average length of time it has taken for a Bear Market to breakeven.9. Returns in the first year after the five biggest market declines ranged from 36% to 137%, and averaged 70%.

These are the facts. Everything else is a scare tactic.

The Stocks vs Companies Game

“It's not a market of stocks. It's a market of companies.” ―Nick Murray

To drive home the companies versus stocks distinction, consider this thought experiment. List ten companies whose products and services your family uses nearly every day.

My Family's Example:1. Apple. We have two Apple laptops and one iPhone.2. Alphabet. Most of our family owns Google Pixel phones and we google stuff a jillion times a day.3. Netflix. Somebody’s always watching something.4. T-Mobile/Mint. The wireless carrier of our phones.5. U.S Bank. We bank there.6. USAA. Carries our personal and business insurance.7. Procter & Gamble. The family consensus is that Bounty is, in actual fact, the quicker picker-upper.8. Amazon. Somebody’s always ordering something.9. Citibank. Many of our credit cards are issued by Citi and are in constant use.10. Berkshire Hathaway. Seems like our lives run on Duracell batteries!

Would I stop using any of these products and services if the stock market went down 50%?No, of course not. And neither would just about anyone else. That’s the critical difference between stocks and companies. Stock prices can crater, and they often do, if only temporarily. But as long as real people continue to buy the products and services of great companies like the ones I’ve just named, they’ll endure. And, if history is any guide, they’ll resume the gradual increase in their earnings and dividends — a process that has delivered an average annual compound 10% return for almost a century.

“We invest in companies for the long-term, not buy stocks for the short-term.” ―this was told to me personally by one of Capital Group's fund managers.

The Method: Equity Mutual Funds

The best way to own the great companies of the world is not to buy them directly, but to own them indirectly via mutual funds.

Equity mutual fund = A broadly diversified, professionally managed collection of the world’s great publicly-traded, mainstream, profit-seeking companies.

Said another way: To own a basket of shares of the world’s most substantial, soundly financed, profitable and innovative global businesses, many of whose products and services we purchase regularly.

“We are long-term owners of well-diversified portfolios of superior companies that have consistently demonstrated their ability, in time, not merely to survive but to triumph over any and every earthly species of ‘crisis.’” ―Nick Murray

An all-equity mutual fund is a professionally managed type of collective investment that pools money from many people and invests it in a large number of companies (usually over 100). The mutual fund hires professional fund managers who choose exactly which companies to buy (and when to sell).A mutual fund is a lot like a pie — no matter how small (or big) a slice you take, you still get the same ingredients.

“My fortune is invested in profit-seeking enterprises managed by largely rational men and women who respond to the reality of price signals every minute of every day. Price signals sent out by seven billion people making economic and financial decisions in their own best interests.” ―Nick Murray

7 Benefits of Equity Mutual Funds

1. Diversification is our Equity SacramentPerhaps the biggest benefit of mutual funds is their massive diversification.One of my most-recommended investments, the American Funds Growth Portfolio, consists of seven individual mutual funds and collectively invests in 1,285 companies from 47 countries among dozens of industries.This provides stability and is the ultimate risk management device.

2. Invest 100% in publicly-traded companies. No bonds, options, futures, precious metals, alternatives, hedges, crypto, or real estate etc.3. Consistent performance. Example: the American Funds Investment Company of America has averaged 12.2% since 1934, net of fees.4. Two layers of the best human thinking. 1) The executives running the companies we're investing into; and 2) the mutual fund managers who decide which companies to invest in.5. Relatively low volatility compared to other investments because they're very diversified.6. Lower stress and maintenance for you. Once you've invested in a mutual fund there is nothing more to do. All investment decisions are made by the fund managers.7. Your money is accessible within five days.

“It can be historically demonstrated that the best defense against retaining your purchasing power through retirement is to invest in a broadly diversified portfolio of the world’s great companies. And the finest method of investing in them are good, long-term mutual funds.” ―Nick Murray

What the Experts Say about Long-Term Equity Investing

This is a selection of my favorite investment quotes, curated over three decades, which capture the essence of my all-equity investment philosophy.

Nick Murray is the Advisor to Advisors and prolific author. With 50+ years of experience in the investment markets he is an expert in the art and science of helping individual investors work toward reaching their investment goals. He is the recipient of the 2007 Malcolm S. Forbes Public Awareness Award for Excellence in Advancing Financial Understanding.

Start by reading Nick Murray's 20 Investment Epiphanies.

“On my 41st anniversary in our great profession, I did a piece for Financial Advisor magazine called “Forty-One Epiphanies,” listing that number of great realizations I'd experienced during those years. This is an excerpt of the 20 epiphanies that are client-oriented." ―Nick Murray

“Successful investing is counterintuitive.”

“I own mainstream equities for two reasons: (1) second only to love, the most powerful force on earth is human ingenuity; and (2) equities are the only asset class that fully captures human ingenuity.”

“The stock market has been going up all your life!”

“The only way to achieve the full permanent advance of equities is to be willing to ride out their full temporary decline.”

“It is those 'risky' equities that provide the greatest long-term safety of principle.”

“Insure against what can go wrong in order to acquire the luxury of investing for what can go right.”

“It's never the wrong time to put some more money with the right money manager.”

“We are long-term owners of well-diversified portfolios of superior companies that have consistently demonstrated their ability, in time, not merely to survive but to triumph over any and every earthly species of 'crisis.'”“No one knows for sure why the equity market does what it does on any random day. And no long-term, goal-focused, patient, disciplined investor cares.”

“Never interrupt the compounding.”

“The average person's rather bizarre view of the stock market is primarily due to a loss of long-term perspective.”

“The patient, disciplined long-term investor has historically been rewarded for standing fast in a crisis.”

“Those who judge their portfolio by its performance relative to some narrow benchmark are focusing on an issue that is largely irrelevant to their ultimate financial success. The only benchmark that you should care about is one that indicates whether or not you’re on track to accomplish your financial goals.”

“The economy is not at all correlated to the markets. It is one of the best fictions of the culture. The culture believes that the economy drives the market and thus is predictive. Wrong. This is one reason why we invest in companies not countries.”

“An intelligently diversified equity portfolio will always 'underperform' some narrow sector of stocks. That's how you know you're truly diversified.”

“The only way you can lose money is to mistake a temporary decline for a permanent loss.”

“Volatility isn't really risk but uncertainty.”

“The economy is not at all correlated to the markets. It is one of the best fictions of the culture. The culture believes that the economy drives the market and thus is predictive. Wrong. This is one reason why we invest in companies not countries.”

“Without an adequately compensated advisor to help with selection and discipline, the individual investor will simply make all the classic and horrendous mistakes.”

“Defend purchasing power with equities, rather than defending principle with bonds (or other fixed accounts).”

“The cardinal tenet of my philosophy is that all long-term investment success comes from acting on a plan, while all failure is precipitated on reacting to the markets.”

“Volatility is merely randomness around a permanent uptrend.”

“EQUITIES: The only asset class that fully captures human ingenuity, which is the most valuable asset on earth.”

“I suggest that perhaps if we checked our actual dividend income every 90 days instead of checking our account balances every 90 minutes, we might become better investors.”

“Permanent loss of capital in equities has no historical precedent. Permanent loss in a well-diversified equity portfolio can only be triggered by an investor's irrational decision to sell in a decline.”

“The dominant determinant of long-term, real-life financial outcomes is not investment performance. It is investor behavior.”

“You must tune this stuff out, it doesn't matter. The economy and government are uncorrelated to the market. Don't make investment policy out of your distaste for the government.”

“Timing the market is a fool’s game, whereas time-in the market is your greatest natural advantage. ”

“Always make investment policy decisions based upon history rather than on headlines.”

“Every crisis has appeared to be totally unprecedented as we were going through it. Just as this one does. This time is no different.”

“I will never own enough of any one thing to be able to make a killing in it. Nor will I ever own enough of any one thing to be able to be killed by it. Diversify.”

“We’re not even investing in “the stock market” as such. Rather, we are investors in companies.”

“Equities are the ideal solution to clients’ need to accumulate enough capital to retire comfortably during their working lives. And then as the ideal (if not the only) vehicle for increasing their income further and further above consumer inflation through three decades of a two-person retirement.”

“Our plan continues to anticipate that at least 20% of our invested capital will appear to disappear temporarily about every five years or so.”

“The Fundamental Retirement Question: Will I outlive my money, or will my money outlive me?The Fundamental Retirement Challenge: To keep my retirement income growing as my cost of living continues to increase.”

“Gold isn't an investment at all, it just sits there. It doesn't produce anything.”

“When stock prices are going down, the enduring value of the underlying companies is going up.”

“Good markets only teach bad lessons.”

“Risk is measured as the probability that you won’t meet your financial goal. Investing should have the exclusive objective of minimizing this risk.”

“We are goal focused and planning driven, in a culture that is market focused and performance driven. We are planning long term, patient, disciplined investors. We build portfolios based upon your goals, we look neither to the left at market volatility, nor to the right at economic news but straight ahead at your retirement.”

“No one knows for sure why the equity market does what it does on any random day. And no long-term, goal-focused, patient, disciplined investor cares.”

“The great truth is that the premium return of equities is earned purely by a willingness to ride out their temporary declines. Yet it is those temporary declines upon which human nature fixates.”

“Volatility is not risk. If you can't sit through a -15% temporary decline every year, and an average -30% temporary decline every 5 years, you have no business being an equity investor.”

“I don’t know what 'the stock market' is going to do over the next 12 months; neither does anyone else. And it doesn't matter.”

“Bull markets go on far longer than bear markets do; they increase equity values far more than bear markets diminish them.”

The economy can’t be forecast. The market can’t be timed. Therefore, the correct time to buy equities for the long run is whenever you have the money. By the same logic, the correct time to sell equities is whenever you need the money. Everything else is commentary.

“Staying fully invested during temporary market declines is the only sure way to capture the entirety of the market’s permanent advance. It is not possible consistently to sell out of falling markets, and later buy back into already advancing markets.”

“The more often you trade, the lower your return. The more often you go in and out of the market, the further below the index your returns will be. Hence we don't do market timing.”

“Never try to make long-term investment strategy out of short- to intermediate-term disruptions.”

“By the time investors become convinced that a crisis has passed, the market will long since have recovered, and they will have missed a huge part of a historic recovery.”

“Today's financial crisis invariably becomes yesterday's news.”

“Every day you hang in there, your reinvested dividends are buying more shares at fire-sale prices from somebody who’s panicking out — who’s making the mistake you refuse to make.”

“The best predictor of the trajectory of a market recovery is the trajectory of the previous decline.”

“No financial, fiscal, monetary, economic or political crisis ever in the history of the world has been capable of inflicting a permanent loss on equity values.”

“Long-term the market is completely predictable. Short-term it is utterly unpredictable. I know two things: 1) The market goes up. 2) The market goes down. I don't know when they happen, nor how long they last (and I don't care).”

“It is the engine that drives the returns. The premium long-term return of equities is simply an efficient market’s way of pricing in their extreme randomness in the short term.Equities pay 10% long-term because in any given year they might be up 20% or down 20%, and you’ll never know which.”

“Dollar Cost Averaging is a strategy in which mutual fund shares are purchased in fixed dollar amounts every month, regardless of the market. Thus, as prices rise fewer units are bought, and as prices fall more units are bought. Dollar Cost Averaging is almost real-time re-balancing.”

“Virtually no portfolio strategy more reliably produces worse returns than performance-chasing.”

“No financial, fiscal, monetary, economic or political crisis ever in the history of the world has been capable of inflicting a permanent loss on equity values.”

“Every crisis has appeared to be totally unprecedented as we were going through it. Just as this one does. This time is no different.”

“We create robust plans by looking back over very long time periods.”

“All the money that has ever been 'lost' in all the temporary equity market declines have always returned to other people: long-term investors with faith in the future; patience, and the discipline to continue working their long-term plan.”